Some essential checks to do before buying any share

Lots of people like the idea of building and looking after their own portfolio of shares. However, when it comes to doing this in real life they often find the whole process rather daunting. When I talk to private investors they often tell me that the one of the biggest problems that they face is the sheer volume of information out there. Many of them feel that they are literally drowning in it and therefore don't know where to begin.

To some extent, I agree. There is a lot of information out there but I'm not sure how much of it is really useful to the long-term private investor. For example, the internet is stuffed full of stock market chatter which has absolutely nothing to do with the long-term prospects of companies and their shares.

One of the steps you need to take in order to become a better investor is to learn to ignore a lot of the noise out there and concentrate on what really matters. That's why I've always spent a long time looking at the financial performance of companies and the stock market valuation of their shares. A focus on numbers allows me to paint my own picture of a company and lessens the chances of me being swayed by someone else's opinion on it.

A couple of days ago, I was asked by a ShareScope customer whether there are just a few key numbers or factors that people should always use when weighing up a share. This is not a simple question to answer. That's because different types of companies require different tools of analysis. For example, you wouldn't use the same set of financial ratios to look at a bank as you would a retailer.

However, despite there being no right answers here, I've come up with some key factors that you can use as a quick ready-reckoner to see if it's worth doing some more research on a company. These checks can be done in a matter of minutes in ShareScope or SharePad.

Phil Oakley's debut book - out now!

Phil shares his investment approach in his new book How to Pick Quality Shares. If you've enjoyed his weekly articles, newsletters and Step-by-Step Guide to Stock Analysis, this book is for you.

Share this article with your friends and colleagues:

A word of warning before I begin

I don't believe that investing can be just reduced to a series of numbers and formulas.

As important as the numbers are, it is vital that you take some time to understand the business behind the numbers. You need to work out important things such as how a company makes money and whether it has a competitive edge that allows it to thrive.

Please don't be put off by this; it doesn't involve hours of research.

I firmly believe that only by understanding the part ownership of a business which a share represents can you hold your nerve and keep calm in the roller coaster world of stock market investing.

When I am beginning to look at a share of a company, I always try and keep in mind that I am trying to answer three very important questions about it:

- Is it a good business?

- Is it safe?

- Is it cheap enough to buy?

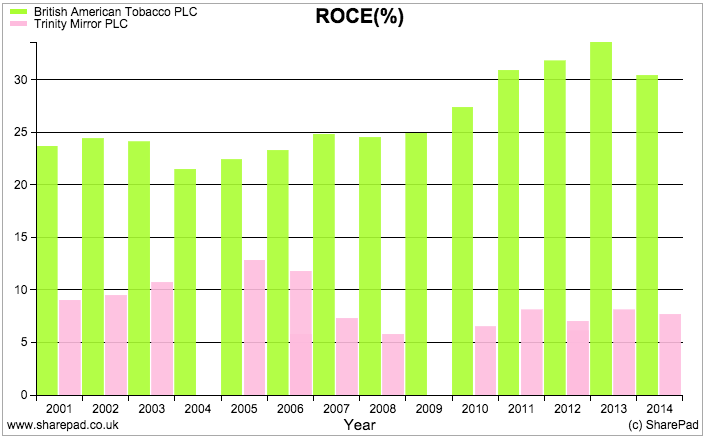

Return on capital employed (ROCE)

Good businesses make lots of money (or profits) compared with the amount of money (capital employed) that has been invested in it. This is why the calculation of ROCE is probably one of the best indicators as to whether a business is any good or not.

Very simply, you can consider ROCE as being the interest rate that a company earns on its investments. Generally, the higher the value the better. It is also important to look at the trend in ROCE. A stable or rising ROCE is much a better indicator of a quality business than one that goes up and down a lot.

Have a look at the chart below: Without knowing anything else, which business would you rather own?

You might be thinking: what is a good value for ROCE? It depends on the industry a company is operating in. As a rough rule of thumb, a ROCE that is consistently more than 15% is a sign of a fairly decent business. Try and compare ROCE with similar companies as well.

Banks and financial companies don't suit ROCE very well due to the way they are financed. With these companies - and perhaps property companies as well - you will be better off looking at return on equity (ROE). Again a figure of more than 15% is reasonable, but bear in mind that companies can juice up their ROE by adding more debt (for an example of this read my Step-by-Step guide here).

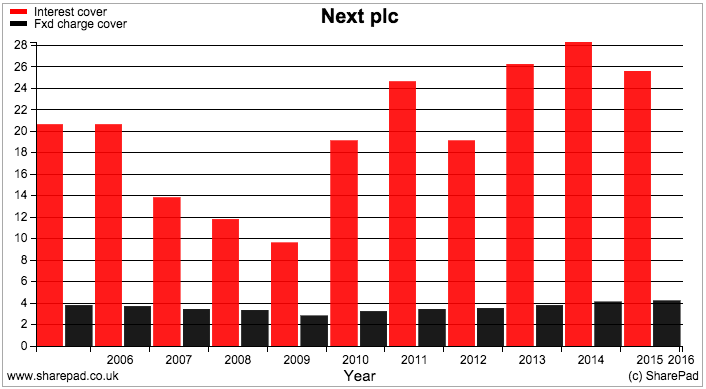

Interest cover/fixed charge cover

With the exception of financial companies and utilities which tend to be financed mainly with debt, it is usually best to avoid companies with lots of debt. This is because a company must pay the interest on any money it has borrowed before it can pay any money to shareholders.

The bigger the interest payments are, the bigger the risks to shareholders. This risk is known as financial gearing. When a company's trading profits are rising, the presence of debt and interest payments magnifies the change in profits after tax (like putting a car or bike in a higher gear) so that profits to shareholders rise by a bigger amount.

However, when trading profits fall this gearing effect works in reverse and can leave shareholders with small profits and sometimes losses.

By looking at the number of times a company's trading profits can cover the interest payments on its debt - its interest cover ratio - you can get a good feeling of the financial risks you are facing as a shareholder. The higher the level of interest cover, the less risky the shares tend to be.

The other thing to bear in mind is that companies can have forms of debt that are hidden from view. This is known as off-balance sheet debt. When companies rent buildings (such as shops or offices) or equipment (such as vehicles) they are usually tied into agreements to pay rent for a period of time. These future rent obligations are just like interest on debt and have to be paid out of profits. But you won't find these liabilities on a company's balance sheet.

If you were to calculate interest cover for a retailer you might think that it is not that risky. The fixed charge cover ratio takes into account the ability of a company to make enough money to pay its rents as well. This ratio would probably have kept you from investing in some high profile retail failures during the last decade such as HMV and Woolworths.

As you can see with Next plc above, the fixed charge cover is much lower than interest cover but both measures are at comfortable levels. Depending on the stability of a company's profits, a fixed charge cover below 1.5 might be a cause for concern.

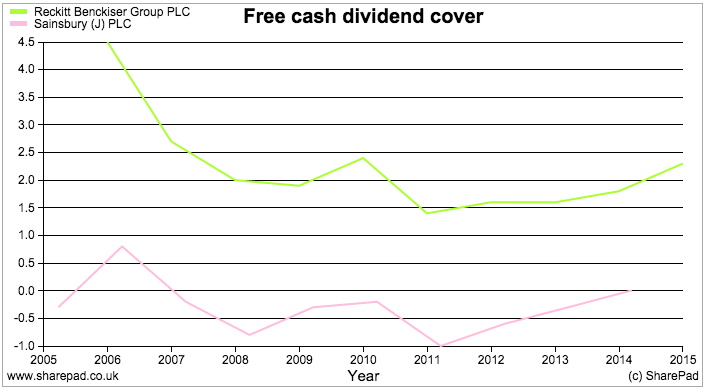

Free cash flow

Sometimes profits aren't what they appear to be. You can find a company that looks very profitable but those profits don't get turned into surplus (or free) cash flow. If you are investing in a share for its dividend then the company paying it needs to have cash left over after all other obligations such as tax, interest and spending on new assets (capex) have been paid.

You can calculate a number of ratios based on free cash flow. Two very useful ones are free cash dividend cover which tells you if dividends are covered by free cash flow and free cash conversion which compares free cash flow per share with a company's earnings per share (EPS) - or how good a company is at turning its profits into free cash flow.

These ratios are best looked at over a period of time such as five to ten years. It's perfectly acceptable for a company to have no free cash flow in some years as long as it is due to it spending money on investments that will produce more free cash flow in the future. If a company has a history of not having lots of free cash flow then this may be a good reason to stay clear of the shares.

Reckitt Benckiser has been able to comfortably pay its dividend from free cash flow - its free cash flow cover ratio has been consistently more than 1. Sainsbury's is a different story and might explain why its dividend has been cut recently. A study of its free cash dividend cover would have been warning you that the dividend was under threat a long time before it was cut.

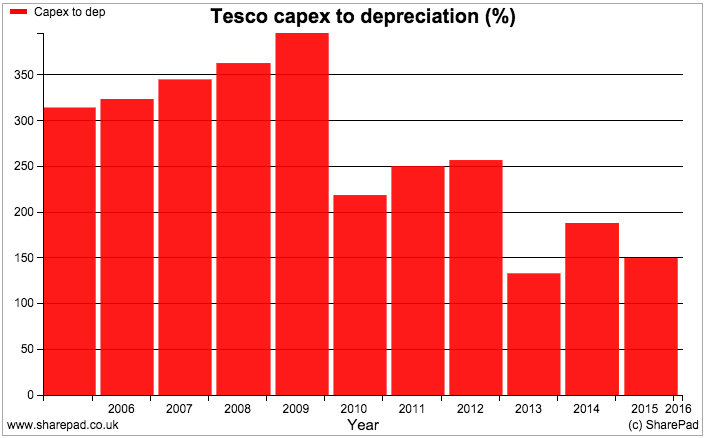

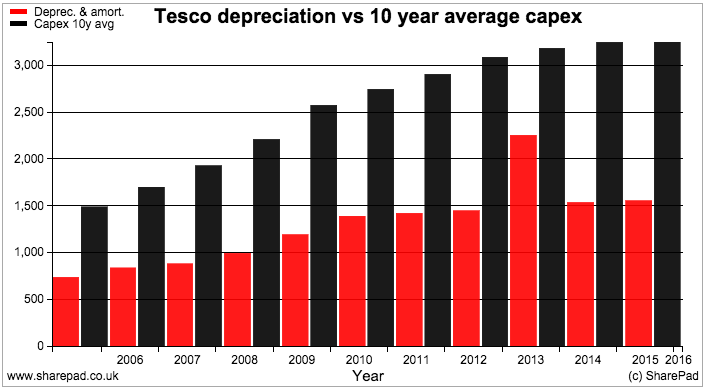

Capex to depreciation

The biggest reason for free cash flow per share to be less than EPS is usually because a company is spending more on new assets than its annual depreciation expense.

Profits are calculated after depreciation has been charged as an expense. Depreciation does not represent the spending of any cash. Cash is only spent when the asset is bought in the first place. Depreciation is used to spread the cost of fixed assets (such as a building or a piece of equipment) over their useful lives. Sometimes it can be seen as an estimate of how much a company needs to spend to maintain the value of its existing assets.

Depreciation is an easy figure to manipulate. The directors of a company can - and do - boost profits - but not cash flow - by extending the useful lives of an asset. That is, by spreading the cost of the asset over a longer period, the annual depreciation charge is lower.

Capex is the actual amount of money spent on new assets in one year. This includes money spent to replace existing assets that have worn out and on assets to expand the business (such as a new factory).

Capex moves up around from year to year depending on the company's investment plans whereas depreciation tends to be more steady. This is why the change in profits from year to year are often more stable than changes in free cash flow.

By comparing capex to depreciation, the investor can get a feel for if a company is spending too much or too little on its fixed assets. When a company is expanding, its capex will be sometimes considerably more than depreciation. However, capex that is persistently higher than depreciation for many years can be a sign that the depreciation expense is too low and that reported profits have been inflated.

In the example above, Tesco's capex has been consistently higher than depreciation (more than 100%).

Very few companies are expanding all the time. Over a period of 5-10 years the amount of money spent on new assets can be expected to even out and could be seen as an estimate of what a company needs to spend to retain its competitive edge.

One very useful tool in SharePad is to compare the depreciation expense with the average amount of money spent on new assets over ten years. If a company's ten year average capex is considerably more than its depreciation charge it might be because it has been investing heavily. It might also be telling you that its profits aren't believable.

It also pays to be wary of companies that have lots of free cash flow but where capex has been considerably less than depreciation. On the one hand, this might be a very good sign if the company has very prudent depreciation policies but more often than not it is a sign that a company is under-investing in its business. Sooner or later it will have to replace its assets and free cash flow will take a dive to lower or negative levels.

Dividend history

Not all companies pay dividends. For those that do, dividends can make up an important part of the returns you receive from owning a share - especially if you reinvest them.

Dividends can be used as a sign of company's health and future prospects as they can only be paid if it has sustainable profits and cash flow. If a company pays a dividend then examining its dividend history can tell you a lot about how robust it might be in the future.

For example, a company that has paid a rising dividend for many years will be seen as a lot safer than one where the dividend has been cut or scrapped. Companies cut dividends for a number of reasons. Sometimes a cut can be explained by mistakes with a previous business strategy where a company overextended itself and took on too much debt. Cutting the dividend in this case frees up cash resources to reduce debt. If a company has learned from its mistakes then hopefully dividends in the future will be a lot safer.

Dividend cuts are also quite common in cyclical companies where profits tend to move up and down in line with the economic climate. These are companies where the past could repeat itself in the future and that banking on a continuous rising stream of dividend payments is by no means certain and something to focus your research on.

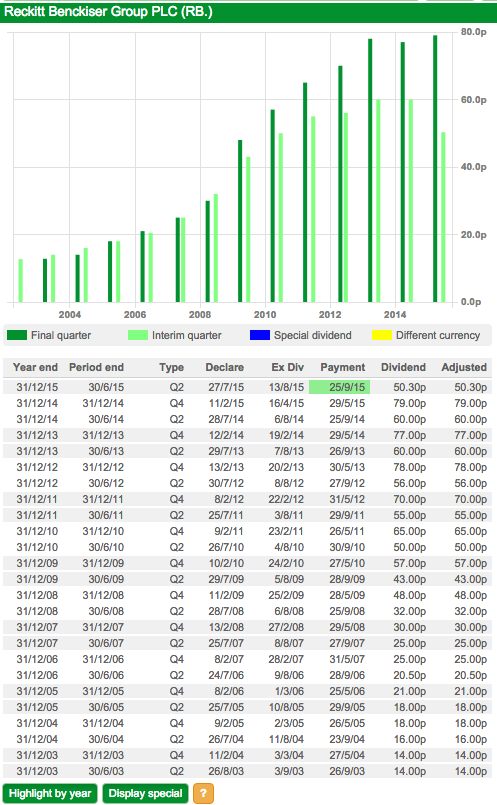

Here you can see that Reckitt Benckiser has been paying a higher annual dividend since 2007. Wolseley, in stark contrast has cut and scrapped its dividend before paying a rising dividend for the last five years.

Also look to see if a company has a habit of paying regular special (one-off) dividends. If they are paid in addition to a regular annual dividend then this might highlight a company's ability to generate lots of surplus cash.

In ShareScope and SharePad it is very easy to study a company's dividend history as shown in the table below (SharePad).

Insider ownership and big shareholders

It's usually a good sign if a chief executive owns a lot of shares in the company they are running. Ideally you want to see the value of their shareholding equal to at least twice their annual pay. This means that they have a meaningful amount of money to lose which will hopefully incentivise them to do the right thing for the company and its shareholders.

You'll often find that the chairman and chief executive of smaller companies can own a significant stake in the business. Elsewhere though it is not uncommon to find them owning very few shares. Also watch out for shares that are granted through share options or management incentive plans which often cost the manager nothing and represent free money. This is not the same as the person buying shares with their own money which is what you want to see.

Director buying and selling can also be a very important indicator of sentiment towards a company. Lots of selling by directors might be a sign that they think the shares are highly priced but can also be for quite acceptable reasons such as paying tax bills or funding a divorce settlement. Large volumes of director buying with their own money is rarely a bad sign for outside investors and usually a sign of confidence in the company.

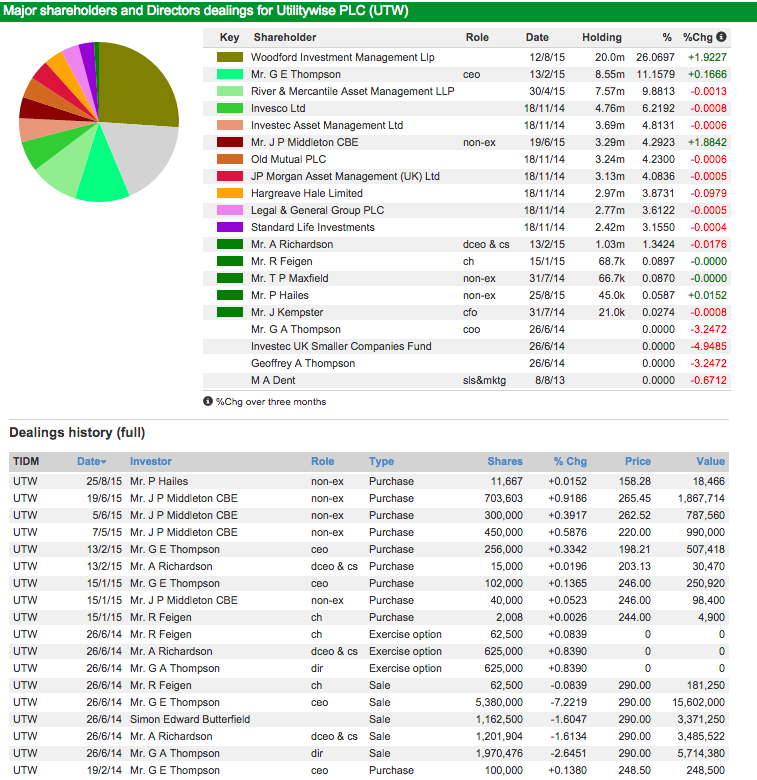

It's also worthwhile looking to see who the big shareholders of a company are. A big shareholding by one or more reputable fund managers might give you some confidence that you could be looking at a decent potential investment. In SharePad you can also see whether these major shareholders have been net buyers or sellers in the previous three months.

Here's an example of AIM-listed share Utilitywise.

Here you can see that the chief executive (Mr G E Thompson) owns just over 11% of the company whilst a non-executive director (Mr J P Middleton) also owns over 4%. Mr Middleton and Mr Thompson have also bought quite a lot of shares this year at much higher prices than the current share price (c 175p in September 2015).

The biggest shareholder is Woodford Investment Management which owns 26% of the company. This investment company is run by Neil Woodford, a fund manager with a very impressive investment track record. It has also been buying shares and has recently increased its stake in the company by 1.9%.

These shareholdings can all be viewed positively but this doesn't mean you should go out and but this share or similar shares. As always, do your own research before buying any share.

The price to pay - the most important check of all

I've left the most important check until last.

All the checks above are all well and good but will be totally wasted if you pay too much for a share. Working out the right value for a share is an art rather than a science and there are many ways to go about it.

Remember, the price you pay for a share determines the returns (changes in share price and dividend yield) that you will get back from it. Blindly paying too much for a great company can often mean that you make no money from its shares.

Choose a method of valuation that you understand and are comfortable with and stick with it. Set yourself upper limits as to what you will pay for a share. For example, you might set the following limits depending on what valuation measure you are using and the type of company you are looking:

- A PE ratio of 15 or less

- A dividend yield of 3% or more

- A price earnings growth (PEG) ratio of less than 1

- A price to tangible book value of less than 1.5

- An EBIT yield of at least 10%

This is just a very small sample of some of the checks you can do when researching a company and its shares. You can find more information on these checks and others in my Step-by-Step Guide to Investment Analysis on the ShareScope website (click here to read more).

If you need help finding any of this information in ShareScope or SharePad, please don't hesitate to call our Customer Support team on 020 7749 8504. Or use the Support Chat group in SharePad.

If you have found this article of interest, please feel free to share it with your friends and colleagues:

We welcome suggestions for future articles - please email me at analysis@sharescope.co.uk. You can also follow me on Twitter @PhilJOakley. If you'd like to know when a new article or chapter for the Step-by-Step Guide is published, send us your email address using the form at the top of the page. You don't need to be a subscriber.

This article is for educational purposes only. It is not a recommendation to buy or sell shares or other investments. Do your own research before buying or selling any investment or seek professional financial advice.